2025 holiday season consumer spending

Looking for the on-demand recording of the Highlight Showcase session, From Gifts to Groceries? Watch (or rewatch) the presentation at this link.

Every year as a part of Highlight's annual virtual summit, Showcase, we use our own Highlight product research platform to conduct original consumer research to share with our audience.

Called From Gifts to Groceries, we use this data to get a pulse check on how consumers are feeling as we enter the holiday season, and compare those results with the previous year’s survey results.

2025's Showcase was held on October 8, and the data for these insights was collected from Highlight's nationwide community of testers (our "Highlighters") in mid-September. Read on to see what insights our Highlighters had to share.

About the Highlighters: our proprietary community of testers

"Highlighter" is the name that we affectionately use for members of our nationwide community.

We pride ourselves on a lower acceptance rate than average because we are so set on finding folks who are earnest, dedicated, and articulate in their responses. For example, our admission survey will contain things like red herring questions to make sure that folks are actually reading the questions and choosing answers carefully. We have open-ended questions to make sure that folks aren't just saying, "No, I don't like this product," but instead are saying, "No, I don't like this product because of X, Y, and Z," giving us those valuable, rich verbatims that our customers have come to value so much.

Our Highlighters love the product testing and research process as well. It is inherently mutually beneficial: For the innovation side, it's incredibly value to know that we're going to develop and put products into the marketplace that are likely to succeed and not end up in landfills. For Highlighters, as consumers themselves, they feel like they have some sense of control over their destiny, that they have some feedback in this process, and that they're able to say state their needs and assist companies in meeting those.

“I realize the importance that honest feedback gives to both companies and their consumers. By being a Highlighter, I feel like I can help both sides to make the perfect product.” - Alyssa

You can learn more about our Highlighters in this blog

About the Highlighters who shared insights for this survey

This year (2025), 2,057 Highlighters completed this survey.

- 53% live in a single income household (vs 52% in 2024)

- There was a fairly even spread of total annual household incomes represented:

- 34% earn < $50k annually

- 35% earn $50k-100k annually

- 31% earn > $100k annually

- Age, by generation, spread as follows:

- 44% Millennial

- 31% Gen X

- 13% Baby Boomers

- 7% Gen Z

- 4% Gen Alpha

- 1% Silent Generation

Year-over-year consumer insights on sentiment, 2024-2025

Consumers are cautious, but consistent

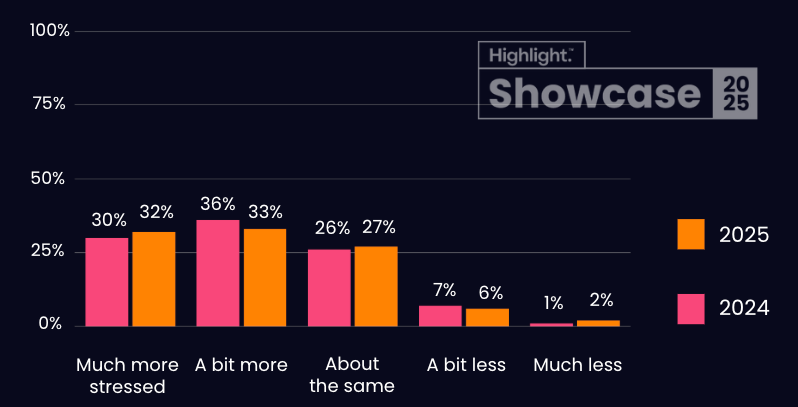

To kick things off, we asked survey takers, "Compared to this time last year (Sept-Dec 2023/2024), how have your stress levels related to money changed?"

Here's what they told us:

In 2024, 66% of Highlighters said they were more stressed about money than the period in the previous year, 65% answered the same in 2025.

While that data may convey a certain amount of fiscal caution, the consistency year over year could also indicate that there exists within the population a steady proportion of folks who are generally concerned about their finances.

The story is the same when it comes to groceries

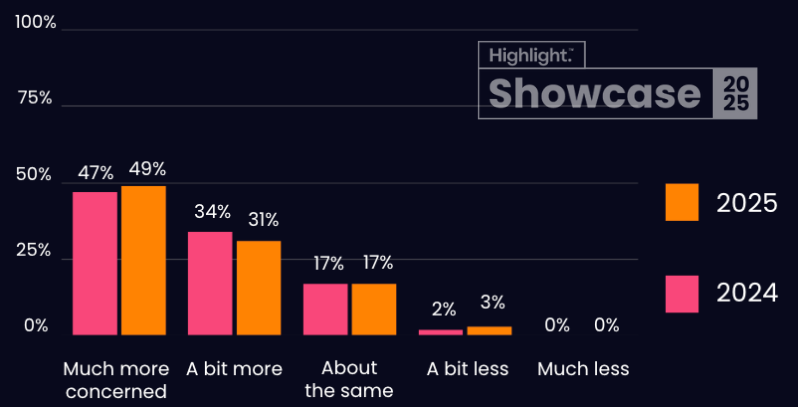

We then asked survey takers, "Compared to how you felt this time last year (Sept-Dec 2023/2024), are you more or less concerned about the cost of groceries?"

Here's what they told us:

In 2024, 81% of Highlighters were more concerned than the period in the previous year, 80% answered the same in 2025.

As with the first question, the year-over-year consistency we see in these responses could convey a continued sense of concern over grocery prices, but it could also indicate that a consistent proportion of shoppers that feel generally concerned about grocery prices.

When it comes to grocery prices, consumers are still adjusting to the new normal

While we can't draw definitive conclusions about the reasons driving this sense of concern about grocery prices among survey Highlighters, we all know as grocery shoppers ourselves that the grocery landscape has changed tremendously over the last five years.

In just these few data points from Pew Research comparing grocery price changes from January 2020 to August 2025, we can see a clear story:

- Meat poultry fish & eggs: +36%

- Eggs alone: +116%

- Cereals & bakery: +29%

- Bread: +30%

- Dairy: +22%

- Fruits & veg: +16%

- Overall average increase: 28% since Jan 2020

While the initial period of inflation following the original COVID pandemic of 2020 has cooled, US consumers are still adjusting to our "new normal" where prices are, on average, 28% higher than they were just a few years ago.

Shoppers are foregoing more “just for fun” purchases

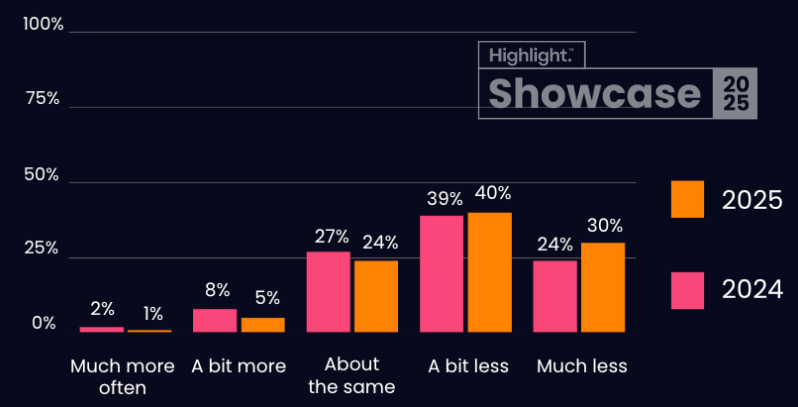

We also asked Highlighters, "Compared to this time last year (Sept-Dec 2023/2024), how have your spending habits on 'just for fun' purchases changed?" Here's what they had to say:

While in 2024, 63% of Highlighters were of Highlighters were making fewer “just for fun” purchases than the same period in the previous year, that number jumped to 70% in 2025.

Consumers say they’re doing less to save

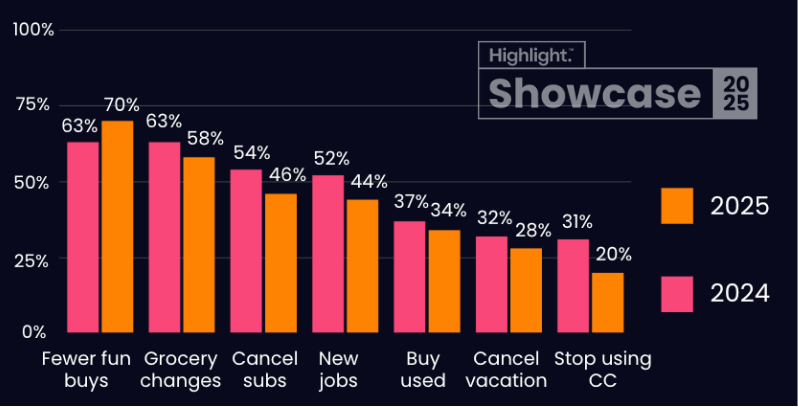

Although a majority of survey Highlighters said they are feeling more stressed about money than the previous year, in this year's results, Highlighters across the board reported doing less to relieve financial stress. (We asked: "In the past 12 months, what have you done to relieve stress related to money? (Select all that apply.)")

As you can see, 70% of Highlighters say they are making fewer "just for fun" buys, and in 2025, Highlighters also said they are:

- Changing the way they grocery shop (58%)

- Canceling subscriptions (46%)

- Looking for new jobs and/or new sources of income (44%)

- Buying secondhand / used (34%)

- Canceling vacation plans (28%)

- Stopping use of their credit card(s) (20%)

From this data, we can consider a few possibilities for the underlying cause of these behaviors and why they have all decreased slightly year-over-year:

1. Perhaps as consumers adjust to our "new normal" where grocery prices - and other costs - are higher, they are already settled into new "budget habits" that are working for them

2. Perhaps consumers have already "pulled" all of these potential "levers" already over the years since 2020 in an effort to relieve financial stress.

To truly understand these underlying causes, we'd have to jump back into the Highlight platform to pursue qualitative research through open-ended questions, video responses, or in-depth interviews with Highlighters - stay tuned for more of that at Showcase 2026!

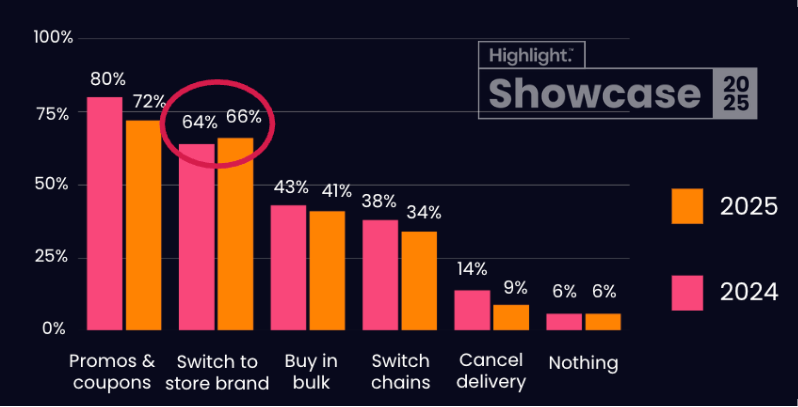

Likewise, consumers are doing slightly less to manage grocery costs in 2025

When we dug more specifically into how consumers are navigating higher grocery prices, we asked Highlighters to share with us, "In the past 12 months, in what ways have you grocery shopped in an effort to save money? (Select all that apply.)" They said:

Highlighters told us they are:

- Promos, discounts and coupons (72%)

- Switching to store brands (66%)

- Buying in bulk (41%)

- Switching to different grocery chains (34%)

- Canceling grocery delivery (9%)

- Doing nothing to try to save on groceries (6%)

As in the previous question, we'd have to dig into qualitative research to really understand the drivers behind these quantitative results (and we will for Showcase 2026!), but one increase that stood out to us - because it was the only increase year over year - was that more Highlighters say they are switching to store brands, giving yet more credence to the headlines around private label that we've been seeing in recent years.

See our interview for Retail Dive with CVS's Vice President of Store Brands

Private label’s power holds firm with shoppers

When it comes to opinions on and perceptions of private label brands and products, we see consumer sentiment and loyalty creep up year over year, as in the following responses:

“I buy store brand products because they’re cheaper than the alternative brand(s).”

90% agreed in 2024

89% agreed in 2025

“I buy store brand products because I like them better than the alternative brand(s).”

25% agreed in 2024

24% agreed in 2025

“Store brands are better value than the alternative.”

45% agreed in 2024

47% agreed in 2025

“Store brands are lower quality than the alternative.”

21% agreed in 2024

19% agreed in 2025

Year over year, we see consumers generally continuing to choose private label with slight increases in affinity in 2025. While a small minority of shoppers say their reason for buying private label is still about price point, more shoppers - nearly half now - are appreciating private label products for their value, and fewer have concerns about quality. A steady quarter of all shoppers said they genuinely prefer the store brand - an encouraging insight to see for those product innovators on the retail side who are working hard to create high value products that shoppers really love.

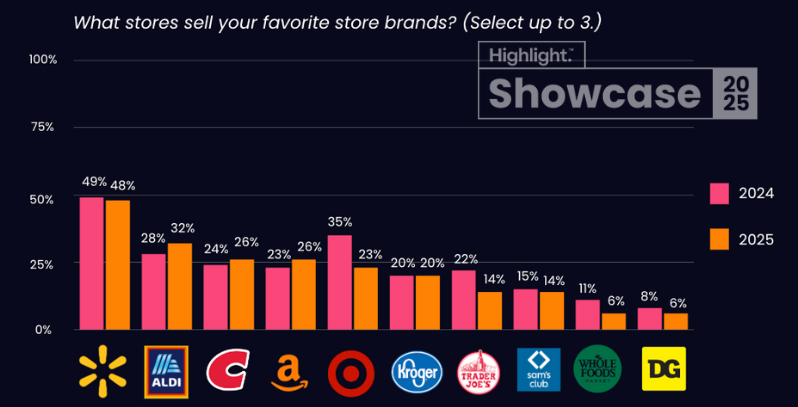

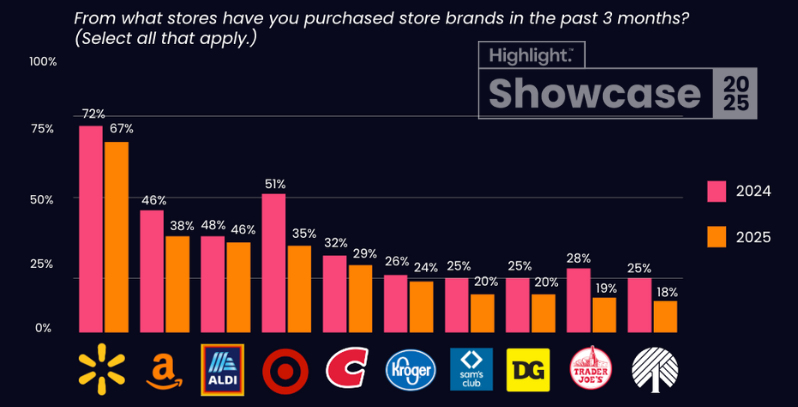

What private label brands do shoppers love the most?

We used a two-part question to learn more about true consumer sentiment on different private label brands as a tactic for bridging the "say-do" gap. First, we asked consumers what stores sell their favorite store brands. Then, we asked from which stores they had actually bought store brands in the past three months. Here's how the ranking fell out, year over year:

When it comes to both stated affinity and actual shopping behaviors, Walmart topped the charts. With its market penetration and years of consistent value messaging, it's no surprise to see its demonstrated popularity amongst shoppers.

Another interesting result to see is the continued and growing popularity of Aldi. While every town in America may have a Walmart, Aldi still has room to grow, and as it spreads across the US, more and more shoppers are getting excited to try their store brands. (As an example of positive shopper sentiment for Aldi, see our session from Highlight Spark, Predicting the Beverage Flavor of the Summer. Aldi's gut healthy soda was a write-in winner.)

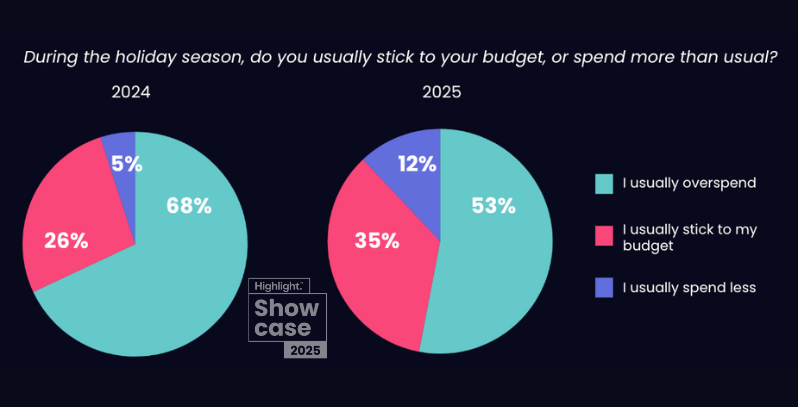

What’s ahead for the holiday consumer spending?

Looking ahead to the holiday season, we asked Highlighters, "During the holiday season, do you usually stick to your budget, or spend more than usual?" This is an interesting question to look at year-over-year results for, because it's less about real, stated behaviors and more about how our perception of ourselves evolve with our environmental conditions.

Here's what we heard from Highlighters:

It's interesting to see such big changes in how consumers see themselves year over year. Once again, this is an area of research that we'd love to dig further into with qualitative methods. But if we can use this opportunity to make an educated guess, this might be a reflection of the continued financial pressure households are feeling, and the desire to see themselves as the kind of person or shopper who makes responsible decisions. The more than double increase in the proportion of Highlighters who even said they "usually spend less" is a real testament to how today's consumers want to see themselves.

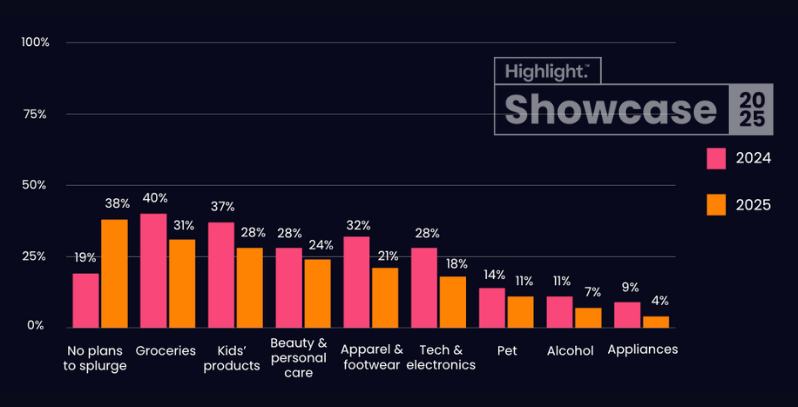

Brands will have to fight for every dollar splurged this holiday season

When we asked Highlighters "In what categories do you plan to splurge this holiday season?" we saw perhaps the biggest year-over-year change of the survey. While in 2024, the answer "No plans to splurge" was the sixth most popular response, it was the top response for 2025.

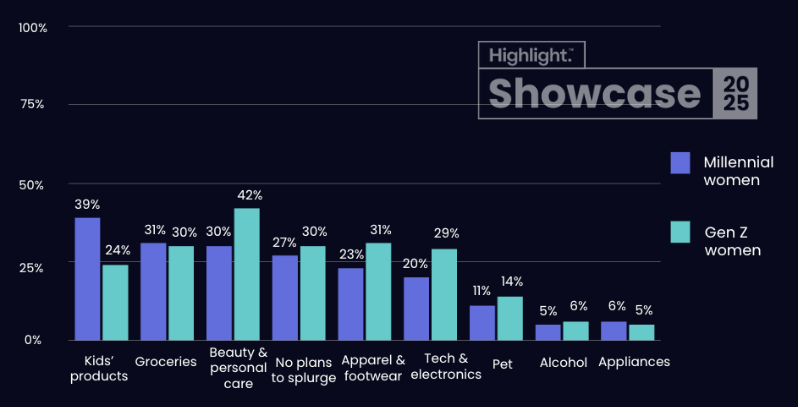

When we segmented responses by two key cohorts: Millennial women vs Gen Z women, we were able to see some interesting insights, including millennial women's plans to splurge on products for children. The younger cohort of Gen Z women, however, are looking forward to splurging on categories perhaps for themselves: Beauty and personal care, and even a significant amount naming "Tech & electronics" as a category they plan to splurge on this upcoming holiday season.

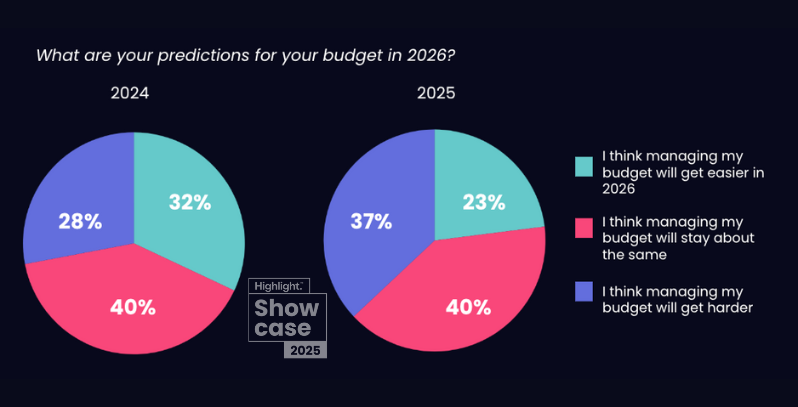

Most consumers remain ambivalent about 2026

When we asked Highlighters to look ahead to 2026 and make predictions about their budget, we saw remarkable consistency in an "ambivalent middle" - 40% both in 2024 and again in 2025 who expect managing their budget to remain consistent in the coming year.

Meanwhile, there was a not insignificant jump in those feeling more pessimistic, with 37% (vs 28% last year) predicting their financial pressures may grow in 2026.

Takeaway for CPG brands: "The point of our business is happiness."

While much of the consumer data remained consistent year over year, we can't ignore the growing pessimism expressed by a significant proportion of survey Highlighters. Those CPG innovators who do ignore this may miss a significant opportunity.

As Whipnotic co-founder Tracy Luckow was quoted in our Showcase Keynote session with Smiley Poswolsky, "The point of our business is happiness." While that's certainly true of her brand Whipnotic, brands in every corner of the CPG world should be taking advantage of their relatively high-velocity categories to be the source of whimsy, escape, and delight that consumers need more than ever.

Yes, consumers are looking for products that function as intended or satisfy a need. But don't miss out on your opportunity to build affinity and real, long-term loyalty with your consumers by bringing moments of joy to their day-to-day shopping and product experiences.

Find more Showcase content

Related reading: The Real Impact of Inflation on Consumer Spending in 2025.